It started with a single Instagram video on May 12, 2026. Noor Shazniah Rahmat, founder of shawls brand Kaise Store, posted about paying S$8,800 to social media agency BrandTok for 20 videos to be done by January 2026. By the end of that month, only three videos had been delivered. Four more came in February. Then nothing. She asked for a prorated refund of S$5,720. BrandTok said no, citing “legal investigations” with no further explanation.

Within 48 hours, other clients came forward with almost identical stories. Daniel Yeow of The Social Space had paid a S$5,250 deposit for a 60-video package. The videos were eventually delivered, but he described them as unusable. Captions had factual errors. The content showed no understanding of his business. He had been verbally promised a refund back in June 2025. It never came. He filed a Small Claims Tribunal claim in August. The payment arrived minutes before the October hearing.

In total, at least 12 businesses paid a combined S$154,550 to BrandTok over roughly a year and a half. Individual amounts ranged from S$1,900 to S$25,000. Three businesses seeking S$39,177 in refunds have been told the money is not available.

Why this happens to Singapore SMEs

Small content agencies in Singapore often run on tight budgets. They depend on client deposits to fund current work. When they grow too fast without the right systems in place, things break down. Existing clients wait longer. New clients get signed to bring in more cash. The gap between what was paid for and what actually gets delivered keeps growing. By the time clients complain loudly enough to get attention, the money is usually already gone.

But operational problems alone don’t explain everything here. BrandTokHoldings, a new company linked to Sam Heedy, was registered in January 2026. This happened while existing client complaints were already escalating. The company kept signing new clients while failing to deliver on current ones. BrandTok’s contracts included no-refund clauses that were used to stop clients from pursuing claims they would likely have won. Verbal refund promises were made but not followed through until clients took legal action.

Bad systems and bad intentions can exist at the same time. The BrandTok story likely involves both. But here is what matters for every SME reading this: the payment structure that made this possible is the same either way. When a client has already paid in full, a failing agency and a dishonest one produce the same result. The money is gone.

The real problem is not what you think

The easy reaction is to see this as a story about one bad agency and move on. That feels safe because it suggests the fix is just better judgment about who to trust. It is not. Character is hard to assess. Payment structure is not.

When clients paid in full upfront, their money went straight into day-to-day operations. When the agency ran into trouble, there was nothing left to refund. The payment structure, not the agency’s intentions, is what left every client without any leverage. Paying everything upfront means you are financing the agency’s operations before they deliver a single thing. If anything goes wrong, for any reason, that money is already spent. You have no way to get it back.

The clients who eventually recovered money had to fight for months through legal channels. One won a tribunal judgment and still has not been paid. The payment structure put every client in a position where they were fighting for money they were already legally owed. That fight was expensive, slow, and in at least one case, still unresolved.

Before you sign: what should your per-video rate actually cover?

Most content agencies quote by volume: X videos for X dollars. That per-video rate sounds straightforward. But producing a single piece of content involves several distinct steps, each with real costs. When that rate is low, something in the list below is being cut. Usually without telling you.

Before you sign, ask the agency to confirm which of these are included in their per-video rate. A reputable agency will answer this clearly and in writing.

Red flags to look out for before you sign

Most BrandTok clients had no obvious reason to suspect a problem when they signed up. The agency had a polished online presence, a well-known case study, and a confident pitch. The warning signs were in the contract terms and payment structure, not in anything visible on the surface. These are the specific things to check before committing to any agency, at any budget.

1 Full upfront payment required, with no milestone structure

Many BrandTok clients paid in full or in a large deposit before a single deliverable was completed. No payment was tied to any milestone. This is the single highest-risk term in any agency contract. Without payments tied to delivery, you have no financial leverage and no way to recover unspent funds when things fall short.

2 A per-video rate that cannot cover the full production cost

Divide the total quoted price by the number of videos. That is the effective per-video rate. Now check it against the components listed in the section above. If that rate cannot realistically cover scripting, filming, editing, captions, and reporting, something will be skipped. A low per-video rate is not a deal until you know exactly what it includes.

3 Deliverables that are not specific in writing

“60 videos” is not a scope. A proper scope specifies format, length, platform, posting schedule, approval process, revision rights, and what “completion” means for each piece of content. Daniel Yeow had no grounds to dispute work he described as unusable because the delivery standard had never been written down. If it is not in the contract with specifics, it does not exist as an enforceable obligation.

4 Case studies you cannot independently verify

BrandTok’s marketing consistently featured one campaign: the social media growth of Kucina Italian Restaurant. Chef Gero later said he was not a paid ambassador and that the results were largely driven by his own ideas. That one reference directly influenced at least one client to commit S$25,000. Before treating any case study as proof, ask to speak directly with the client featured. A real track record has more than one story. If every conversation comes back to the same name, ask why.

Once work starts: two patterns to act on immediately

5 Explanations for delays that keep changing

One BrandTok client was told delays were due to health issues. Then it became staffing problems. Then cash flow collapse. When explanations keep changing and each one is worse than the last, the agency is managing your expectations rather than the actual problem. A real operational issue comes with a revised plan. Escalating excuses without a plan are a different signal entirely.

6 Delivered work that shows no understanding of your business

Several BrandTok clients received videos with factual errors in captions, grammatical mistakes, and content that made it clear the agency had not understood their product or audience. If the first deliverable arrives that far from the brief, it is almost never a one-off problem. Raise it formally, in writing, straight away. Poor first delivery is almost always a sign of something deeper.

If it has already happened: your real options

If you are already in this situation, there are legal routes available. Each one comes with a real limitation worth understanding before you commit time and money to it.

All of these options share the same core problem. If there is nothing left to recover, a legal win does not mean you actually get paid. Prevention is always cheaper than the fight.

How to protect your payments to any social media agency in Singapore

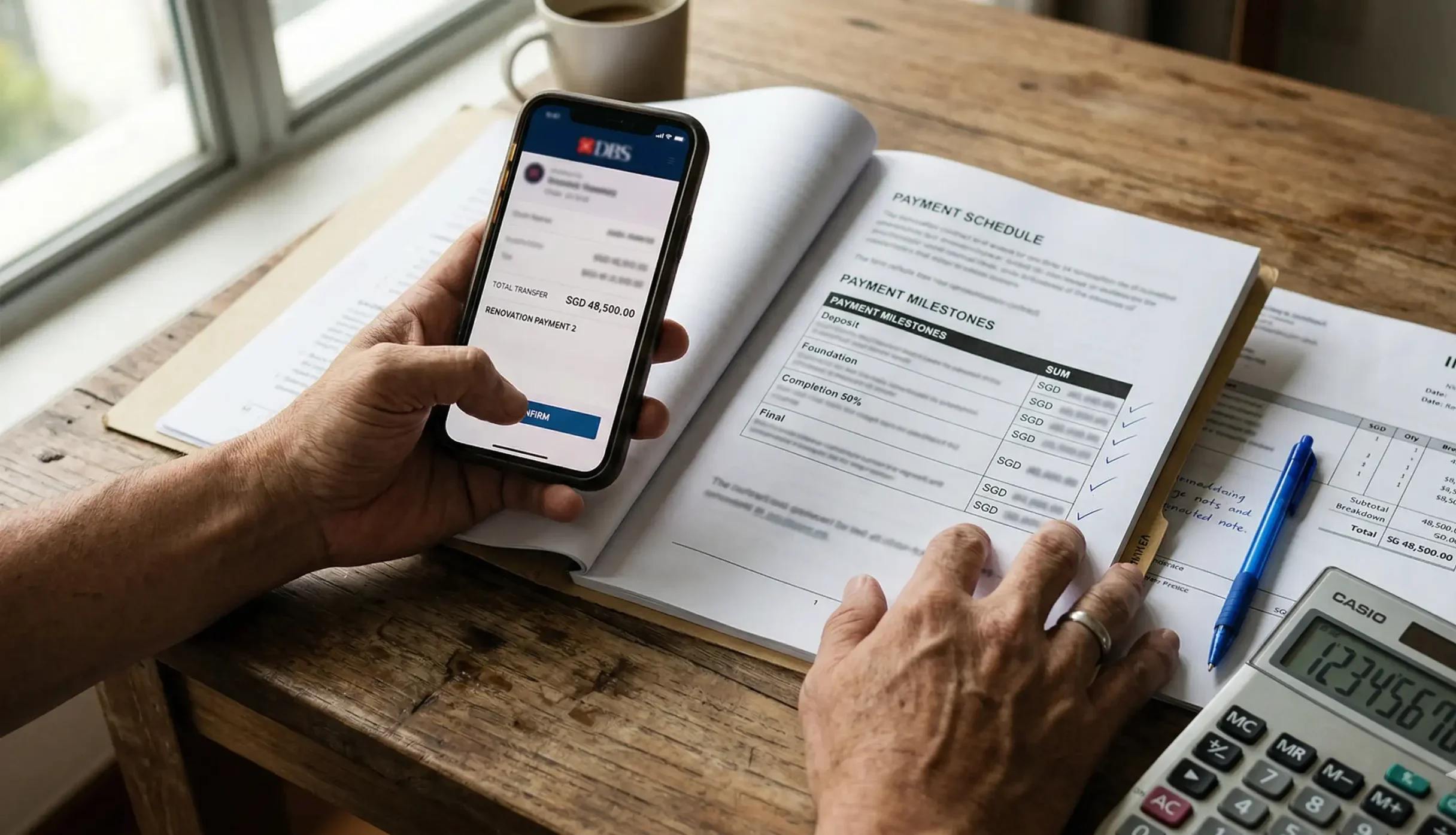

The answer is not better intuition about which agencies to trust. It is removing trust from the equation entirely when it comes to money. Escrow-based milestone payments do exactly that. Your funds are committed to the project but held independently, in a custodian account, until you confirm each milestone is complete. The agency cannot access money it has not yet earned. You cannot walk away without consequence either. Both sides are accountable to the structure, not to each other’s goodwill.

This is how Handshake works. Before the project starts, you and the agency agree on a milestone schedule. Your funds go into an escrow account held at DBS, completely separate from Handshake’s own operations. When the agency completes a milestone, they notify you for review. You confirm the work is done, and the payment for that milestone releases automatically. If the milestone is not met, the funds stay in escrow. You keep the leverage to pause, renegotiate, or exit, without having already paid for work that was never delivered.

Payments through Handshake are regulated by the Monetary Authority of Singapore. Escrow accounts are held at DBS. It works the same way whether you are working with an agency you have known for years or one you are hiring for the first time. It turns every agency relationship from a trust exercise into a structural agreement. Trust still matters. It just no longer has to be the only thing standing between you and a loss.